The Magnificent 7: Understanding the Risks of Overconcentration in Mega-Cap Tech Stocks

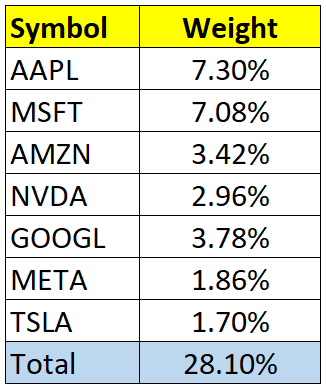

In the current investment landscape, the S&P 500 index has become heavily dominated by seven large technology companies — Alphabet (GOOGL), Amazon (AMZN), Apple (AAPL), Meta Platforms (META), Microsoft (MSFT), NVIDIA (NVDA), and Tesla (TSLA). Collectively branded as the "Magnificent 7," these stocks now account for approximately 30% of the index’s total market capitalization. This concentration poses significant diversification challenges for investors, raising concerns about the potential risks linked to such overexposure.

Market Dynamics and the Rise of the Magnificent 7

The Magnificent 7 have thrived in an environment characterized by low interest rates and heightened enthusiasm for artificial intelligence technologies. Their stocks have driven nearly two-thirds of the returns in the U.S. equity index over recent years, highlighting their significant influence on market movements. However, the very factors that propelled their rise could also contribute to their vulnerability.

From a historical perspective, such levels of concentration are rare. The last two instances of similar dominance by a handful of stocks occurred in the late 1990s and late 2010s. Each time, the subsequent reversal was both severe and prolonged, underscoring the potential risks of overconcentration (BlackRock Insights).

Risks of Overconcentration

The primary risk associated with the Magnificent 7's dominance is the reduced effectiveness of the S&P 500 as a diversification tool. When a few stocks wield outsized influence, the index becomes more vulnerable to volatility. Should these companies face unfavorable macroeconomic conditions or fail to meet investor expectations, the implications for portfolios heavily invested in the index could be significant.

Lisa Shalett, Chief Investment Officer at Morgan Stanley Wealth Management, emphasizes, "Concentration in a handful of stocks reduces the index's diversification potential, leading to larger-than-expected portfolio swings" (Morgan Stanley Wealth Management).

Moreover, the current macroeconomic environment is marked by increased uncertainty, including potential interest rate hikes and evolving trade policies, both of which could impact the high valuations of these tech giants. The heightened sensitivity to economic shifts could exacerbate the risks for investors relying on passive index strategies.

Mitigating Risks through Diversification

To mitigate the risks associated with overconcentration, investors can explore several strategies:

-

Equal-Weighted Index Investment: One alternative to the traditional market-cap-weighted S&P 500 is the equal-weighted version of the index. This approach assigns equal weight to each stock, thus reducing the dominance of any single company or sector. Historical data suggests that the equal-weighted index tends to outperform the cap-weighted one in periods following high concentration levels (Morgan Stanley Global Investment Committee).

-

Active Management: Engaging in active management allows investors to selectively adjust their portfolios, capitalizing on undervalued opportunities and reducing exposure to overvalued segments. This can be particularly effective in navigating volatile markets and mitigating concentration risks.

-

Sector Diversification: Expanding investments beyond the technology sector can provide a buffer against sector-specific downturns. Sectors with cyclical growth prospects, such as financial services, energy, and industrials, may offer compelling opportunities for diversification.

Looking Ahead

As the market progresses into 2025, the trajectory of the Magnificent 7 remains a focal point for investors. While their momentum has been formidable, the potential for a shift in market leadership looms large. The broader market's performance, particularly among the other 493 stocks within the S&P 500, could present attractive alternatives for investors seeking to balance their portfolios.

Tony DeSpirito, Equity CIO at BlackRock, highlights the importance of selectivity in the current environment, stating, "The end of the age of moderation requires investors to be more discerning, as alpha becomes increasingly critical to outcomes" (BlackRock Insights).

In summary, while the Magnificent 7 have undeniably shaped the current investment landscape, their dominance also underscores the risks of overconcentration. By employing strategies such as equal-weighted index investments, active management, and sector diversification, investors can position themselves to navigate potential market shifts and achieve more balanced exposure. As always, a nuanced approach tailored to individual risk tolerance and investment goals remains paramount in managing these risks.