The steel and iron ore markets, integral components of the global economic framework, are currently navigating a multifaceted environment where optimism is tempered by harsh realities. As industrial demand and infrastructure investments rise, so does the hope for sustained growth in these sectors. However, this optimism is increasingly challenged by supply chain disruptions and stringent environmental regulations, which threaten to impede the sector's momentum and influence global economic growth patterns.

Rising Demand and Infrastructure Investments

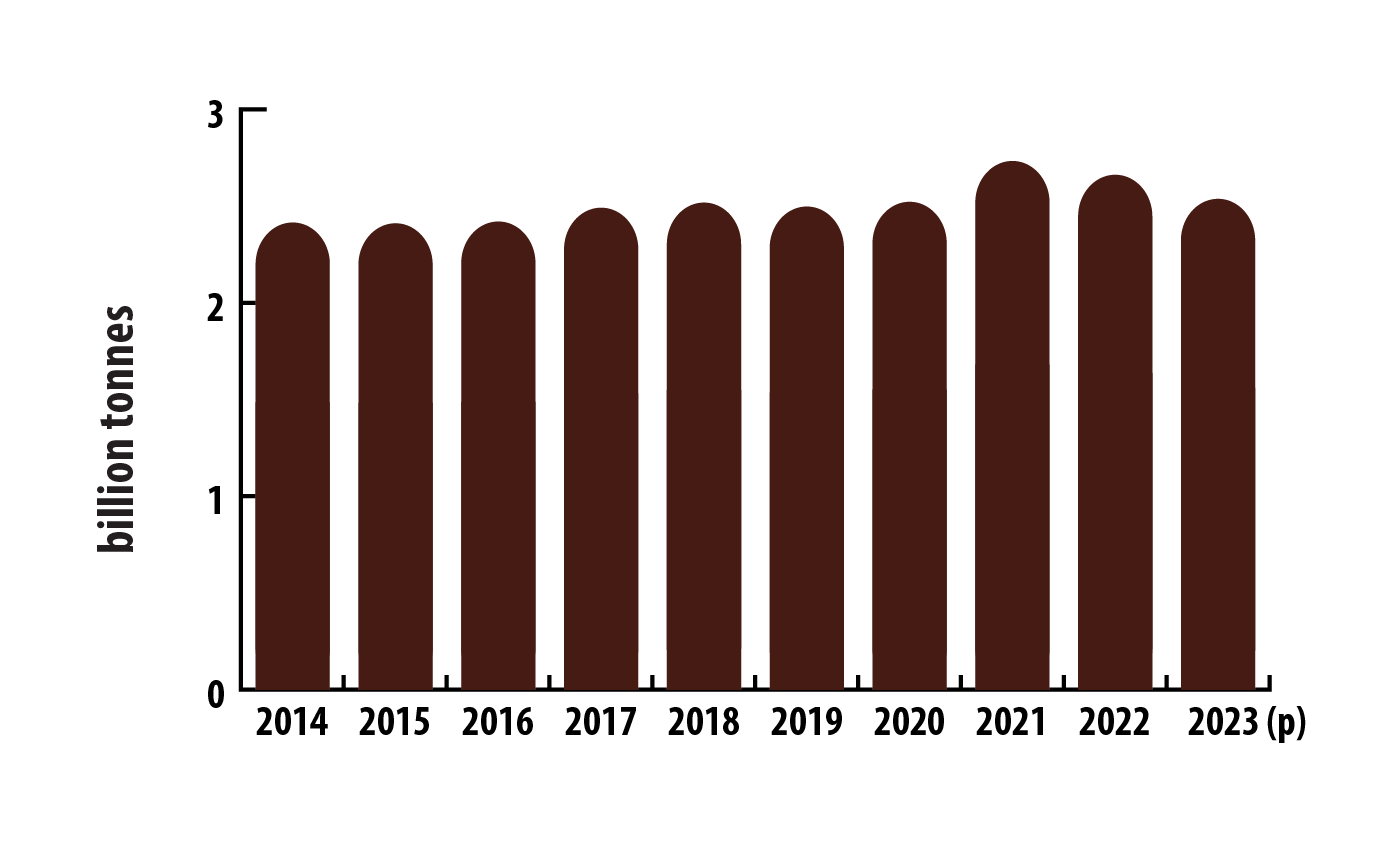

The steel market is buoyed by a resurgence in global infrastructure projects, particularly in emerging economies where urbanization and industrialization are pivotal to economic strategies. The demand for steel is predicted to grow by 2.5% annually, driven by projects like China's Belt and Road Initiative and the United States' infrastructure overhaul plans. According to the World Steel Association, steel production reached approximately 1.9 billion tonnes in 2024, marking a 3% increase from the previous year. This growth is propelled by robust construction activities and the automotive industry's recovery post-pandemic.

In parallel, iron ore, a critical raw material for steel production, has seen a surge in demand. Brazil and Australia, the primary suppliers, have reported exports rising by 5% and 4% respectively, reflecting global market needs. The Australian Department of Industry, Science, Energy and Resources estimates that the global iron ore trade will exceed 1.5 billion tonnes in 2025.

Environmental Regulations: A Double-Edged Sword

While demand growth offers a promising outlook, the sector faces significant challenges from environmental regulations aimed at reducing carbon footprints. The European Union's carbon border adjustment mechanism is slated to impose tariffs on carbon-intensive imports, including steel, by 2026. This move is part of broader efforts to combat climate change but could potentially increase the cost of steel production, impacting global competitiveness.

China, the world’s largest steel producer, has vowed to cap its steel production to reduce emissions. This policy shift has already led to a 4% reduction in production rates in 2024, according to China’s National Bureau of Statistics. These regulations, while environmentally prudent, pose a risk to the stability and predictability of supply, forcing companies to innovate and adapt rapidly.

Supply Chain Disruptions

The steel and iron ore markets are also grappling with persistent supply chain issues exacerbated by geopolitical tensions and the COVID-19 pandemic's aftereffects. The Russia-Ukraine conflict has disrupted supply routes, with sanctions impacting Russian steel exports and limiting access to critical mining resources. Furthermore, logistical bottlenecks at global ports, compounded by labor shortages, have delayed shipments, increasing costs and reducing margins for producers.

Expert Insights and Market Predictions

Industry experts suggest a cautious approach moving forward. According to Alex Russell, a commodities analyst at S&P Global Commodity Insights, "The balance between demand and regulatory compliance will define the market's trajectory over the next decade. Companies that can innovate within these constraints will likely emerge stronger."

The iron ore market, traditionally seen as a steady investment, is now considered more volatile. The International Monetary Fund predicts that while prices may remain elevated in the short term, a correction could occur if global economic conditions falter or regulatory pressures intensify.

Strategic Adaptations

To mitigate risks, companies in the steel and iron ore sectors are investing in technology to improve production efficiency and reduce emissions. "Green steel" initiatives, utilizing hydrogen and renewable energy, are gaining traction, with major players like ArcelorMittal and POSCO leading pilot projects. Additionally, strategic partnerships and mergers are becoming common as firms seek to secure raw material supply chains and share the burden of compliance costs.

The steel and iron ore markets are at a crossroads, where the potential for growth is as tangible as the hurdles they face. Navigating this landscape requires a balanced approach, considering both the hopeful outlook provided by rising demand and the grim realities of regulatory and supply chain challenges. For investors and stakeholders, understanding these dynamics is crucial to making informed decisions in an increasingly complex global market landscape.